Why do some apps give me instant insurance approval, and others take days?

Instant insurance approval explained: the digital underwriting platform mechanics and risk scoring API decisions that separate same-session approvals from multi-day reviews.

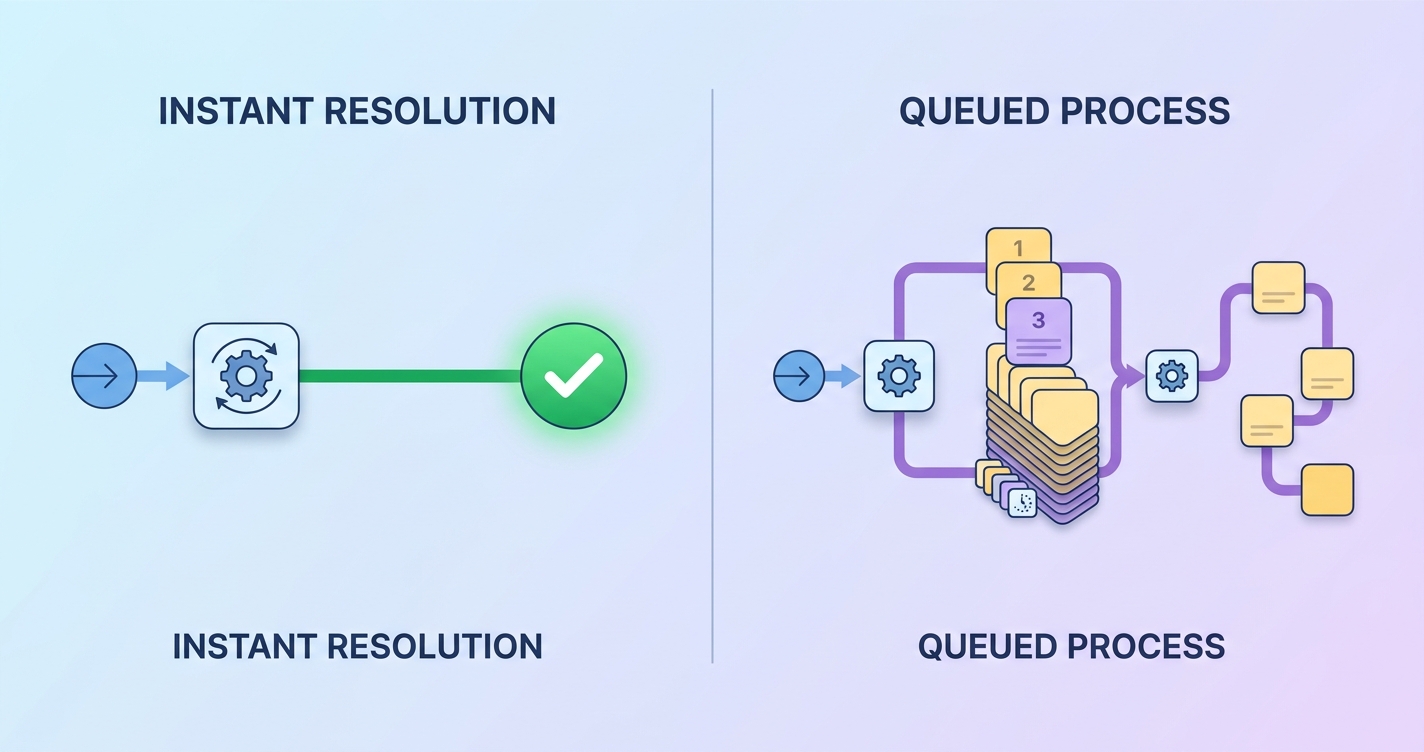

The gap between an app that approves a policy in 90 seconds and one that emails "your application is under review" three days later is rarely about who has the better brand. It is almost always about architecture. For the teams building these systems, instant insurance approval explained correctly is a story about data readiness, decision orchestration, and how many human handoffs a workflow tolerates before it stalls. The same applicant, with the same health profile, can hit a wall at one carrier and sail through another because the two platforms made very different engineering choices about when and how risk gets scored.

Underwriters traditionally spend 30 to 40 percent of their time on administrative tasks, and some carriers now report straight-through processing rates of 50 percent or more for eligible applicants, according to industry analysis summarized by EasySend (2024) and ReMark's review of automated underwriting.

Instant insurance approval explained: what actually happens between submit and decision

When an applicant taps submit, a digital underwriting platform either has everything it needs to decide right then, or it does not. Instant approval is the outcome of a pipeline where every required input arrives in machine-readable form, every risk rule can run without waiting on a person, and every external data call returns inside the user's session. Delay is the outcome of any single dependency that cannot resolve in real time.

There are four broad categories of work happening in that window:

- Identity and data capture. The platform confirms who the applicant is and collects declared health information, plus any device-based signals such as a vitals scan.

- Third-party enrichment. The system queries external sources like prescription history, motor vehicle records, or medical databases through APIs.

- Risk scoring. A model or rules engine converts all inputs into a risk class or a numeric score.

- Decision orchestration. A decision engine maps that score against the carrier's appetite and either issues, declines, refers, or routes to manual review.

Instant decisions happen only when all four stages complete synchronously. The moment one stage goes asynchronous, for example an enrichment source that returns results in 48 hours instead of 400 milliseconds, the whole case drops into a queue and the applicant gets the dreaded "we will be in touch" message.

The real reasons approval times diverge

Two apps can look identical to a consumer and behave completely differently underneath. The table below maps the architectural choices that drive the split.

| Factor | Instant approval path | Multi-day review path | | --- | --- | --- | | Data acquisition | Declared data plus real-time signals captured in-session | Requires paramedical exam, labs, or attending physician statement | | Risk scoring | Underwriting risk scoring API returns a score in milliseconds | Manual review by an underwriter against reference manuals | | Third-party data | Synchronous API calls with sub-second responses | Batch pulls or sources with 24 to 72 hour turnaround | | Decision logic | Automated decision engine with clear accept and decline thresholds | Edge cases routed to a human for judgment | | Coverage band | Lower face amounts inside automated appetite | High face amounts triggering mandatory review rules | | Data quality | Clean, structured, validated payloads | Missing fields, ambiguous disclosures, reconciliation needed |

The pattern is consistent. Instant approval is not a feature you buy. It is the absence of blocking dependencies. The platforms that win on speed have engineered every common case so that nothing in the path has to wait on a slow input or a human signature.

A few specific triggers reliably push a case from instant to delayed:

- Face amount above the carrier's automated underwriting limit, which often forces a fluid or exam requirement.

- A flagged disclosure, such as a recent diagnosis, that no rule can clear automatically.

- An enrichment source that times out or returns a partial result, forcing a fallback to manual.

- Conflicting data, where declared information does not match a third-party record and must be reconciled.

Industry Applications

For underwriting system vendors

Vendors selling into carriers live and die by straight-through processing rates. A platform that automates 60 percent of cases is dramatically cheaper to operate than one stuck at 25 percent. The differentiator is how cleanly the risk scoring layer plugs into the decision engine. When scoring runs as a real-time underwriting risk scoring API rather than a nightly batch job, the vendor can promise instant decisions for a defined, expanding slice of the book.

For insurtech CTOs

CTOs are usually balancing two competing pressures: the growth team wants more instant approvals to lift conversion, and the actuarial team wants to avoid mispricing risk. The resolution is almost always better data at the point of capture. A predictive underwriting vitals signal collected during the application, rather than weeks later in a clinic, lets the platform decide more cases in-session without widening the risk band it is willing to auto-accept.

For BPO providers

Business process outsourcers carry the manual review load that instant systems shed. Their economics improve when the upstream platform classifies cleanly, because every case that auto-decides is a file they never have to touch. Insurance health data integration that arrives structured and validated reduces the per-file handling cost that defines BPO margins.

Current research and evidence

The shift toward synchronous decisioning is well documented. The global insurtech market reached roughly 25.97 billion dollars in 2024 and is projected to expand sharply through the early 2030s, per market analysis cited across industry coverage including Strategic Market Research (2024). Much of that investment targets the underwriting stack specifically, because that is where the friction and cost concentrate.

ReMark's State of Automated Underwriting work has tracked carriers moving from pilot programs to production automation, with many setting internal targets of 70 percent or higher straight-through processing for eligible applications. The COVID-19 period accelerated this measurably, as Swiss Re's automated underwriting analysis noted, when in-person paramedical exams became impractical and carriers needed exam-free pathways almost overnight.

What the research consistently shows:

- Speed is a function of how much data can be captured and scored without human intervention, not raw compute.

- The largest remaining delays come from external data dependencies and high-value cases that rules cannot clear.

- Embedded health signals collected at application time are one of the few levers that expand the instant-decision band without raising risk exposure.

The technical takeaway for builders is that latency lives at the integration seams. A risk model can score in milliseconds, but if it waits on an enrichment call that resolves overnight, the applicant still waits overnight.

The Future of instant insurance approval

The next phase is less about faster models and more about richer real-time inputs. As more signals move into the application session itself, the share of cases that can be decided instantly grows without the carrier loosening its appetite. Three directions stand out:

- Embedded health checks at signup, where an embedded insurance health check captures vitals during onboarding rather than referring the applicant out.

- Continuous and dynamic scoring, where a risk profile can be refreshed rather than treated as a one-time snapshot.

- Standardized health payloads, where formats like FHIR reduce the integration friction that currently forces fallbacks to manual review.

The carriers and vendors that treat instant approval as an architecture problem, rather than a marketing claim, will keep widening the gap. The ones still bolting automation onto exam-dependent workflows will keep sending applicants those three-day emails.

Frequently asked questions

Why did I get instant approval on one app but a multi-day wait on another?

The two platforms made different engineering choices. The instant one likely captured everything it needed in your session and scored it in real time. The slower one probably required an external input, such as an exam, lab result, or a third-party record that does not return immediately, which dropped your case into a review queue.

Does instant approval mean the underwriting was less thorough?

Not necessarily. Instant decisions run the same risk rules a human would, just automatically and only for cases that fit cleanly inside the carrier's defined appetite. Cases that fall outside those automated thresholds are deliberately routed to people, which is what creates the delay.

What makes a case fall out of the instant path?

Common triggers include a face amount above the automated limit, a health disclosure that no rule can clear on its own, conflicting data between what you declared and a third-party record, or an enrichment data source that is slow or unavailable.

Can collecting vitals during the application speed things up?

Yes. When predictive underwriting vitals are captured in-session through a real-time API, the platform has more to score immediately, which lets it auto-decide more cases without widening the risk it accepts. That is one of the few levers that increases instant approvals and protects pricing at the same time.

Circadify is building in exactly this space, with a real-time, vitals-based underwriting risk scoring API designed to keep more decisions inside the applicant's session rather than in a review queue. Teams evaluating how a synchronous scoring layer fits their decision engine can explore the API docs and sandbox at circadify.com/custom-builds.